Ever since mankind bartered with each other for whatever they lacked, or needed, money, as the medium of exchange, has witnessed multiple milestones in its evolution. The Lydians pioneered the minting of gold and silver coins, and the Chinese, under the Mongolian rule, introduced to the Europeans, through Marco Polo, the usage of paper money, which was later known as banknotes when European banks began the issuance of paper money.

Up to the 21st century, cash transactions with banknotes as the medium of exchange remained undisturbed until the emergence of mobile payments and virtual currencies as a part of the development of the financial technology. Transactions have become less of a hassle ever since, and of course, at the cost of the declining use of physical money.

The technological revolution proved to be disruptive to the conventional methods of banking and payment. Traditionally, banks have been the primary source of access to financial services, with services ranging from payment transactions to borrowing and insurance (PwC, 2016, p.8). When the world experienced an exponential growth in technology in the late 20th century, rapid and sudden changes have been taking places in various fields of industries all across the globe.

The payment industry is second to consumer banking in the financial sector in terms of the most likely to be disrupted by FinTech in the upcoming 5 years (PwC, 2016, p.8). Notice that this forecast took place in 2016 in which over $24.7 billion investment in FinTech startup companies have already been made across the globe in 1076 deals (KPMG, 2016, p.6). In a mere couple of years, the amount of the investment made hit the value of $57.9 billion in 875 deals (KPMG, 2018, p.4).

Also, payment services companies are among those in the top-tier rank in FinTech 100; positioned 2nd with a number of 18 payment services companies in 2016, and managed to reach the top rank with 32 companies in 2018. Now that these facts are laid out in the open, what does that mean for us anyway? How does that affect us in any way?

There has been trends that are affecting how the world engage and exchange in business, and how transactions are shifting from cash to contactless, wearables, and even some yet to be realized cutting-edge technologies such as facial recognition. As FinTechs thrives and third-party payment services providers are popping up one after the other, banks can no longer survive unless they learn to collaborate in an open system.

There are demands from consumers for a personalized, agile, and real-time based payment services, and because FinTech places its client at the centre of its business model, enriching customer experience through open-Application Programming Interface (API) banking, utilization of Blockchain, mobile wallets, etc. Security reasons are also becoming a major driver for consumers in shifting partially from cash transactions to mobile payments.

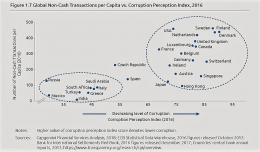

Cash, despite its 85% share in total retail transactions (MasterCard Advisor's Cashless Journey, 2013, p.1), is vulnerable to theft and fraud, takes time to get our hands on, and, well, gives us a cramped wallet, whereas mobile and electronic payments incorporate the distributed ledger technology- yes, Blockchain, exactly-in recording the transactions, Due to its decentralized nature, meaning it is under no directives of any third-party institutions, and the cryptographic security measures, Blockchain ensures that tampering to the records is almost impossible, almost, if you'd like a crack on it, we wish you a good luck.

Another important aspect that need and should be taken into account is the macro drivers for emerging markets that are affecting the payment landscape. PwC Emerging Markets Report 2016 released three macro drivers, stemming from a combination of digital natives expectations and the desire of governments to reduce the use of cash.

First off, a favourable demographics with 85% of the world's population residing within the emerging market countries implies that even a modest market development in a fast growing economy is extremely significant. Also, nearly 90% of the world's under-30 population reside within the emerging markets, and approximately 75% of this age segment accounts for the most online transaction, according to a PwC research in India.

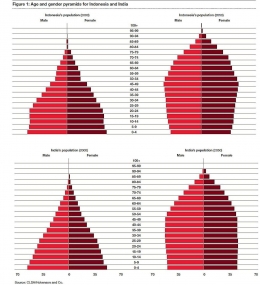

Indonesia's and India's bulging age pyramids suggest that the main online transacting population in the 15-34 years of age segment will move to the next age level over the next 10 years, increasing the online transaction by 15%. This age segment also possesses a strong appetite for technology and has transformed something that was formerly a convenience into an essential of how people transact.